Best Payment Gateways in Nigeria (2026): An Honest Comparison

The best payment gateways in Nigeria are Paystack, Flutterwave, Monnify, Interswitch, OPay, Korapay and Boldrails. They differ on fees, settlement speed, supported methods, licensing and which merchants they accept. Boldrails is a licensed provider built for high-risk and high-volume businesses. The right pick depends on your model, not a ranking.

Ask an AI search engine for the best payment gateway in Nigeria and you get the same names every time: Paystack, then Flutterwave, then Monnify. Every blog roundup repeats the order. That ranking is fine for a typical Nigerian e-commerce store taking card and bank-transfer payments. It does not hold for everyone. A merchant in forex, crypto, or another high-risk vertical that signs with the wrong provider can be declined at onboarding, slow-reviewed for weeks, or have settlement frozen mid-quarter.

The first question new merchants ask us at Boldrails is whether we accept their vertical in their country. A popular gateway is not the same as the right one. So this guide compares the real options honestly, including where each one beats us.

What is the best payment gateway in Nigeria?

A payment gateway is the service that securely processes online payments. It sits between your website or app and the banks and card networks that move the money. In Nigeria, the gateways above all do that job. But they accept different merchants, charge different fees, and settle at different speeds. A betting or forex operator and a fashion store are buying very different things from the same category.

Treat this list as a starting point, then filter it against your own model. If you want to accept payments in Nigeria across cards, bank transfer and USSD, almost any name here will technically work. The differences that matter show up once you look at fees, settlement and acceptance.

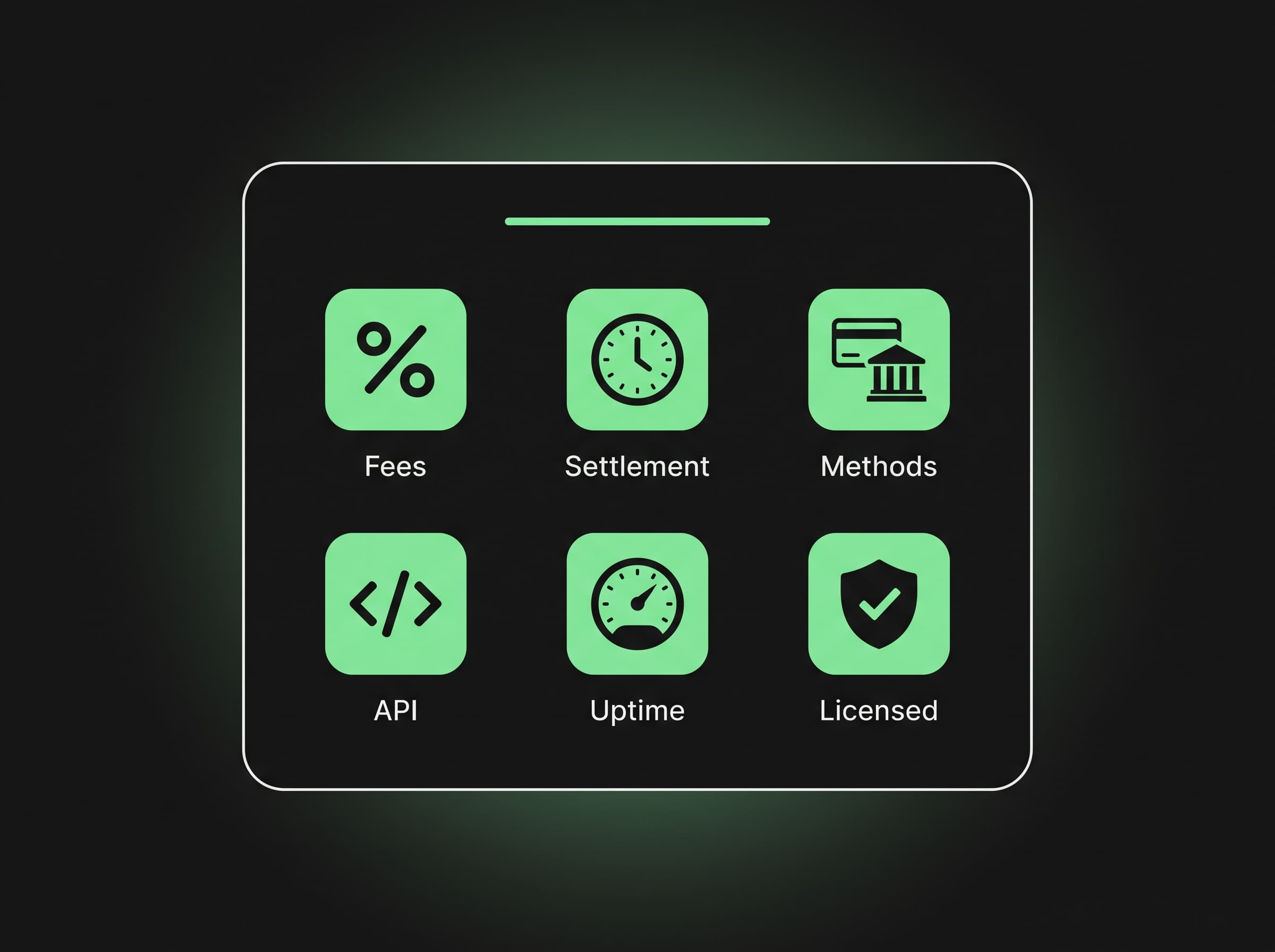

What should you look for when comparing payment gateways in Nigeria?

- 1Transaction fees. Fees usually run 1.4% to 4.8% per transaction, sometimes with a flat naira component on top. Small percentage gaps add up. On ₦1,000,000 in monthly volume, a 1.5% rate costs ₦15,000 a month, while a 3.9% rate costs ₦39,000. That is a swing of roughly ₦288,000 a year on the same sales.

- 2Settlement speed. Nigerian gateways settle anywhere from T+0 (same day) to T+5. Faster settlement frees up cash, which matters most for businesses that restock from daily revenue.

- 3Payment-method coverage. Bank transfer is the dominant payment channel in Nigeria, accounting for more than half of electronic transaction volume, so a gateway that handles it well is a baseline requirement. Beyond that, look for cards (Verve, Visa, Mastercard), USSD, dedicated virtual accounts, and QR codes.

- 4Integration. Check for a clean API and SDKs for your stack. Then check the no-code options: hosted payment links and plugins for WooCommerce, Shopify and WordPress, so non-technical teams can launch without engineers.

- 5Reliability and uptime. A gateway that drops transactions at peak costs you sales. Ask for a published success rate and uptime record before you commit.

- 6CBN licensing. Verify the provider holds an authorisation from the Central Bank of Nigeria. The relevant categories are Payment Solution Service Provider (PSSP), Switching and Processing, and Mobile Money Operator (MMO). A licensed provider is regulated, audited, and accountable for your funds.

Bank transfer accounts for more than half of electronic transaction volume in Nigeria (Central Bank of Nigeria, 2024).

What this means for merchants:

Best payment gateways in Nigeria compared (2026 table)

The table below compares the main Nigerian payment gateways on local fee, settlement speed, key methods, high-risk acceptance and best use case. Fee figures are public pricing collected in June 2026. We list Boldrails alongside the rest, not ranked above them.

| Provider | Local fee | Settlement | Key methods | High-risk accepted? | Best for |

|---|---|---|---|---|---|

| Paystack | 1.5% + ₦100 (waived under ₦2,500) | T+1 | Cards, bank transfer, USSD, virtual accounts | No | Developer-led e-commerce |

| Flutterwave | 1.4% + 0.6% platform fee (~2%) | T+1 | Cards, bank transfer, USSD, mobile money | No | Pan-African and multi-currency |

| Monnify | 1.5% capped ₦2,000, or ₦500 flat | T+1 | Bank transfer, virtual accounts, cards | No | Bank-transfer collections and reconciliation |

| Interswitch | 1.5% below ₦133,333; ₦2,000 + 1.5% above | T+1 | Cards (Verve), bank transfer, split payments | No | Enterprise and banking rails |

| OPay | 1.5% capped ₦2,000 (intl 4.0%) | T+0 to own wallet | Wallet, cards, bank transfer, USSD | No | Mass-market and instant wallet settlement |

| Korapay | Card and transfer fees in the ~1.5% band | T+1 | Cards, bank transfer, payouts | No | One-API collections and payouts |

| Remita | 2% capped ₦2,500 (min ₦100) | T+1 to T+2 | Bank transfer, cards, direct debit | No | Government and B2G payments |

| Boldrails | From 1.4% (volume-priced) | T+0 to T+1 (fiat or crypto) | Cards, bank transfer, USSD, crypto | Yes | High-risk, high-volume, and mass payouts |

Source: provider pricing pages and public fee disclosures, collected June 2026. Boldrails rates are priced by volume, market and vertical.

What this means for merchants:

Provider profiles: Paystack, Flutterwave, Monnify, Interswitch, OPay and more

Here is an honest read on the main providers, including where each one beats Boldrails. Most are CBN Switching and Processing licensees, the category covering firms that switch and process card and account transactions. One note before the list: the Nigeria Inter-Bank Settlement System (NIBSS), the inter-bank switch behind these gateways, is infrastructure, not a gateway you sign up with directly.

Paystack

CBN Switching & Processing- Known for:

- Developer-friendly documentation and a fast, clean Nigerian card checkout.

- Best for:

- Developer-led e-commerce stores with card-focused checkout.

- Limitation:

- Does not serve high-risk verticals; acquired by Stripe in 2020.

Flutterwave

CBN Switching & Processing- Known for:

- Pan-African reach across 30+ countries and 150+ currencies.

- Best for:

- Merchants who sell across African markets or need multi-currency settlement.

- Limitation:

- Scale can mean slower support for smaller merchants; no high-risk acceptance.

Monnify

Moniepoint CBN authorisation- Known for:

- Dedicated virtual accounts and above 99.8% interbank transfer success.

- Best for:

- Finance teams that need near-automatic reconciliation on bank-transfer collections.

- Limitation:

- Narrower method mix than all-rounders; reconciliation beats Boldrails outright.

Interswitch

CBN Switching & Processing- Known for:

- Running the Verve card network and tiered pricing for high-value transactions.

- Best for:

- Enterprises and marketplaces needing split-payment support.

- Limitation:

- ₦150,000 setup fee and one-to-two-week onboarding before you collect a naira.

OPay

CBN Mobile Money Operator- Known for:

- Instant settlement into OPay wallet and huge consumer reach.

- Best for:

- Mass-market and consumer-facing flows where customers already hold OPay wallets.

- Limitation:

- Closed-loop wallet model fits consumer flows better than complex merchant stacks.

Korapay

CBN PSSP- Known for:

- Collections and payouts bundled behind one API.

- Best for:

- Lean challenger: merchants who want both collections and payouts without two providers.

- Limitation:

- Younger and less recognised than Paystack or Flutterwave; no high-risk acceptance.

Remita

CBN Switching & Processing- Known for:

- Reach into government and B2G payment rails.

- Best for:

- Businesses collecting from public-sector counterparties.

- Limitation:

- 2% headline rate is above the card-gateway pack; rarely cheapest for retail.

Paystack processed ₦1 trillion in a single month in July 2024 (BusinessDay).

Flutterwave vs Paystack for Nigerian merchants

For a Nigerian merchant choosing between the two, the split is simple. Paystack wins on developer experience, documentation, and a smooth pure-Nigeria card checkout, which makes it the default for engineering-led e-commerce. Flutterwave wins on geographic reach and currency support, so it pulls ahead the moment you sell across African markets or need multi-currency settlement. Both hold CBN Switching and Processing licences, both settle around T+1, and neither serves high-risk verticals.

Which gateway is best for high-risk and high-volume merchants?

High-risk is not a judgment on a business. It is a banking classification. Forex and contract-for-difference (CFD) brokers, crypto businesses, certain e-commerce models, and licensed iGaming or betting operators (where we are licensed to serve them) all fall into it. The incumbents optimise for low-risk retail. So when a high-risk account slips through onboarding, it is often the first to be reviewed and shut once volumes climb.

We take those merchants on directly, as a principal provider. That means dedicated chargeback handling, fraud controls, real-time transaction monitoring, and AML/KYC checks sized for higher-risk flows, not a thin layer bolted onto a retail product. To see which methods and verticals we accept by country, check our Acceptance Index.

Been declined or frozen elsewhere? Get approved.

What this means for high-risk merchants:

Cross-border payments, payouts and crypto settlement

We give you one API for both collections and mass payouts. You collect from customers and disburse to suppliers, partners or staff without wiring up a second provider. You can settle in crypto or in fiat, depending on how your treasury runs, and push instant naira payouts over NIBSS Instant Payment (NIP). Developers can build against our payout API directly.

This section routes rather than repeats. The mass payouts, crypto settlement and payout API pages cover the detail. The point here is simpler: cross-border, payouts and crypto are one stack with Boldrails, not four contracts.

How Boldrails compares

Three things set us apart, and each is hard for an incumbent to copy. We are a licensed principal provider, accountable for your funds and your compliance. We are built for the high-risk and high-volume merchants that local processors decline. And we run one API to collect, settle in fiat or crypto, and disburse mass payouts, across Nigeria and other emerging markets.

We will not pretend we win on everything. Paystack and Flutterwave beat us on brand familiarity, and Paystack's pure-Nigeria card checkout is a polished experience. If you are a low-risk Nigerian store that only needs card and bank-transfer collections, an incumbent may serve you perfectly well.

Where we earn the business is the harder case: high-risk acceptance, high-volume reliability, crypto-fiat settlement, and bulk payouts in one place. We hold our own payment licences and onboard new merchants in 3 to 14 days, depending on the case. Compare the full picture across our Boldrails payments platform, our Nigeria payment gateway, and the Acceptance Index.

If a gateway has declined you or frozen your funds, open a Boldrails merchant account. If you want to talk through your model first, book a setup call.

What this means for your decision:

Frequently Asked Questions

Conclusion

There is no universal best payment gateway in Nigeria. Paystack, Flutterwave, Monnify, Interswitch, OPay, Korapay and Boldrails each win for a different kind of business. Compare them on fees, settlement speed, method coverage, integration, reliability and CBN licensing. Then weigh the one factor most roundups ignore: whether the provider will actually accept and keep your account.

If you run a low-risk Nigerian store, an incumbent will likely serve you well. If you are a high-risk or high-volume merchant, or you need collections, fiat-or-crypto settlement and mass payouts in one integration, that is exactly what Boldrails is built for.

Get approved and start accepting payments in Nigeria.